Blog Details

Diskava. Beta. Kava

11May

Why Health Insurance Premiums Are Not the Same for Everyone in Kenya

Health insurance is one of the most misunderstood products in Kenya.

Many people ask:

“Why is my medical insurance premium higher than someone else’s?”

“Why did my friend get a cheaper quote?”

“Why is this cover expensive yet the inpatient limit is the same?”

“Why can’t everyone pay one standard amount?”

The truth is simple: medical insurance is not a one-size-fits-all product.

Even when two people are asking for the same inpatient limit — for example KSh 750,000 inpatient cover — the premium can still be different depending on age, hospital panel, benefits selected, health history, family size, location, and the insurance company offering the cover.

That is why comparing health insurance is very important before buying.

At Imana Insurance Agency Kenya Ltd and MyKava Online Insurance Consultants, we help clients compare different medical insurance options, understand the benefits, check hospital panels, review waiting periods, and choose a cover that fits their budget and health needs.

Why Health Insurance Premiums Differ in Kenya

When people hear “medical insurance,” they often assume it should work like buying airtime or paying for a standard service. But health insurance is priced based on risk.

Insurance companies ask themselves:

How likely is this person to need medical treatment?

How much is that treatment likely to cost?

Which hospitals are they likely to use?

Do they already have medical conditions that require regular care?

What benefits are included in the cover?

The higher the expected medical cost, the higher the premium is likely to be.

That is why two people can both request KSh 750,000 inpatient cover, but one person pays less while another pays more.

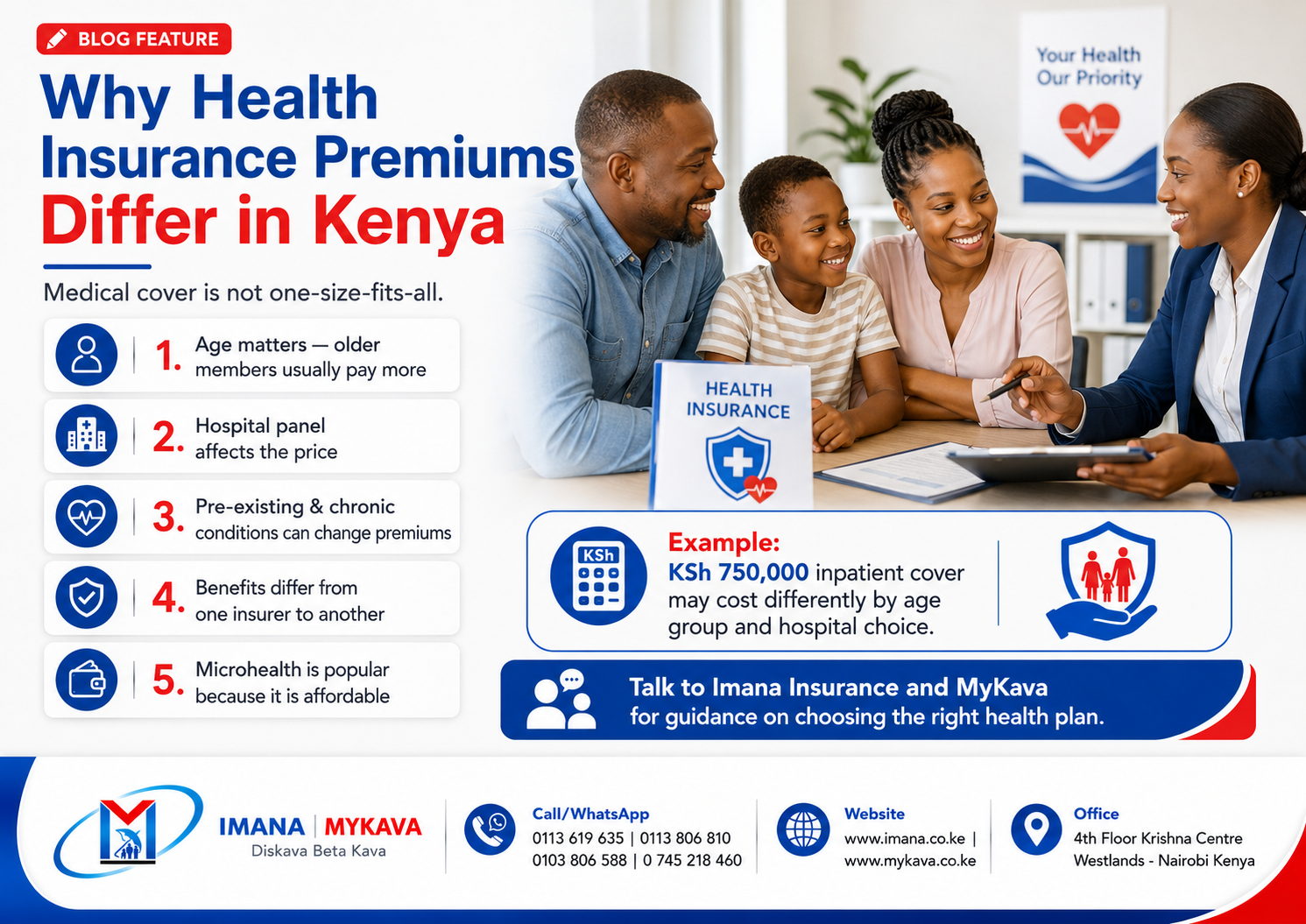

1. Age Affects Medical Insurance Premiums

This is one of the biggest factors.

Generally, the older a person is, the higher the health insurance premium becomes.

This is because older people are more likely to visit hospitals, require tests, need medication, undergo procedures, or manage lifestyle and age-related conditions.

For example, a child, a young adult, a 45-year-old, and a 65-year-old may all request the same inpatient limit of KSh 750,000, but they will most likely not pay the same premium.

A younger person may pay less because their expected medical risk is lower. An older person may pay more because the likelihood of hospitalization or chronic condition management is higher.

This is not discrimination. It is how medical insurance risk is calculated.

2. Hospital Panel Determines the Price

Not all hospitals cost the same.

A cover that allows you to access high-end private hospitals will usually cost more than a cover with a smaller or more affordable hospital panel.

For example, if you choose a hospital panel with premium hospitals in Nairobi, Mombasa, Kisumu, Eldoret, Nakuru, or even regional hospitals across East Africa, your premium may be higher.

Why?

Because the cost of treatment in those hospitals is usually higher.

A consultation, admission, surgery, lab test, scan, maternity service, or specialist review may cost more in one hospital than another. Insurance companies factor this into the premium.

So, when someone says:

“I want the best hospitals but I want the cheapest premium,”

that may not always work. The hospital panel you choose directly affects the price.

3. Pre-Existing and Chronic Conditions Matter

A pre-existing condition is a medical condition someone had before buying the insurance cover.

Examples may include:

- Diabetes

- High blood pressure

- Asthma

- Cancer history

- Kidney conditions

- Heart-related conditions

- Arthritis

- Ulcers or other recurring conditions

- Previous surgeries or ongoing treatment needs

If someone has a chronic or pre-existing condition, the insurer may charge a higher premium, apply waiting periods, offer limited cover, or request more medical information before approval.

This is because the insurer already knows there is a higher chance of medical claims.

That is why it is very important to be honest when applying for medical insurance. Hiding medical history can cause problems later during claims.

Insurance works best when the client and insurer are clear from the beginning.

4. Different Insurance Companies Price Differently

Medical insurance premiums also differ from one insurance company to another.

One insurer may offer a lower premium but with a smaller hospital panel. Another may offer a higher premium but with better benefits, wider access, better chronic condition support, or stronger customer service.

This is why the cheapest plan is not always the best plan.

A good medical insurance decision should look at:

- Premium payable

- Inpatient limit

- Outpatient benefit

- Hospital panel

- Maternity benefit

- Dental and optical benefits

- Chronic illness support

- Waiting periods

- Exclusions

- Claim process

- Customer support

- Renewal terms

Sometimes a slightly higher premium gives you better value. Sometimes an affordable microhealth plan is enough depending on your current needs and budget.

That is why comparison matters.

5. Counties and Countries Can Affect Pricing

Where you live or where you want to access treatment can also affect your medical insurance plan.

A person looking for cover mainly within Kenya may not need the same plan as someone who wants access across East Africa or internationally.

Hospital costs also vary across regions.

A person in Nairobi who wants access to major private hospitals may have different needs from someone in a smaller town who mainly wants access to county-level or mission hospitals.

This is why medical insurance should be guided by real-life usage.

Ask yourself:

Where do I normally seek treatment?

Which hospitals are near me?

Do I travel often?

Do I need East Africa cover?

Do I need international medical insurance?

Your answers can affect the type and cost of cover you should buy.

6. Benefits Selected Also Change the Premium

A medical insurance plan can include different benefits.

For example:

- Inpatient only

- Inpatient plus outpatient

- Maternity

- Dental

- Optical

- Last expense

- Chronic condition support

- Emergency evacuation

- International treatment

- Personal accident benefit

The more benefits you add, the higher the premium is likely to be.

For example, someone buying inpatient cover only will likely pay less than someone buying inpatient plus outpatient, maternity, dental, optical, and chronic condition benefits.

This is why one person may say:

“I got a cheaper quote,”

but when you check properly, their benefits may be fewer or their hospital panel may be smaller.

Cheap is not always cheap. Sometimes it simply means less cover.

7. Family Size Affects the Premium

A single person will not pay the same as a family of five.

Every additional member increases the risk and therefore affects the premium.

A family medical cover may include:

- Principal member

- Spouse

- Children

- Sometimes parents or senior dependants depending on the insurer

Children may have different pricing from adults. Older dependants may attract higher premiums. Some insurers may also have age limits for dependants.

So, when buying family medical insurance, it is important to give correct ages for every member. A quote cannot be accurate without age details.

8. Why Microhealth Is Becoming Popular in Kenya

Many people in Kenya now prefer microhealth insurance because it is more affordable and easier to start with.

Microhealth plans are designed to give basic but useful medical protection at a lower cost compared to traditional full medical insurance.

They are popular among:

- Individuals

- Families

- SMEs

- Chamas

- Welfare groups

- Self-employed people

- Parents buying cover for children

- People who want supplementary cover alongside SHA/SHIF

Microhealth may not give the same wide benefits as high-end medical insurance, but it gives many people a practical entry point.

For many households, the real question is not:

“Can I afford the most expensive cover?”

The real question is:

“What level of medical cover can I afford now, and how can I improve it over time?”

That is where microhealth becomes useful. It gives people a starting point instead of remaining completely uninsured.

Example: KSh 750,000 Inpatient Cover Can Have Different Prices

Let us say three people all want KSh 750,000 inpatient medical cover.

Person A is 25 years old and wants a standard hospital panel.

Person B is 45 years old and wants a wider private hospital panel.

Person C is 62 years old and has a chronic condition.

Even though all three are asking for the same inpatient limit, their premiums may not be the same.

Why?

Because their risk levels are different.

Person A may be cheaper because they are younger and lower risk.

Person B may pay more because of age and preferred hospital panel.

Person C may pay even more because of age and existing medical history.

Same inpatient limit. Different risk. Different premium.

That is why medical insurance must be quoted properly.

Why You Should Not Buy Medical Insurance Blindly

Health insurance is not something to buy casually because someone forwarded a cheap poster on WhatsApp.

Before buying, you should understand:

- What is covered

- What is not covered

- Which hospitals you can visit

- Whether outpatient is included

- Whether maternity is included

- Whether chronic conditions are covered

- Waiting periods

- Age limits

- Claim procedure

- Renewal conditions

- Whether dependants are included

A cheap cover that does not work when you need it is expensive in the long run.

A good cover is not just about the lowest premium. It is about whether the cover can actually help you when sickness knocks.

Why Work With Imana Insurance and MyKava?

At Imana Insurance Agency Kenya Ltd and MyKava Online Insurance Consultants, we help you compare medical insurance plans from different insurance providers so you do not buy blindly.

We help you understand:

- Affordable medical insurance options in Kenya

- Microhealth plans

- Family medical covers

- Children’s medical insurance

- Senior medical insurance options

- SME and group medical insurance

- Inpatient and outpatient benefits

- Hospital panel differences

- Waiting periods and exclusions

- Chronic and pre-existing condition considerations

The goal is simple: help you compare, understand, buy, and save.

You do not need to know all the insurance jargon. That is our work. Your work is to ask questions before buying.

For medical insurance and health cover options, you can visit:

- Imana Health Insurance: https://imana.co.ke/insurance/imana-health

- Health Insurance in Kenya: https://imana.co.ke/insurance/health-insurance

- Microhealth Quote: https://imana.co.ke/micro-quote

- Corporate Medical Quote: https://imana.co.ke/corporate-quote

- Last Expense Quote: https://imana.co.ke/last-expense-quote

- Contact Imana: https://imana.co.ke/contact-us

- MyKava Online Insurance Consultants: https://www.mykava.co.ke

- Imana Insurance Agency Kenya Ltd: https://www.imana.co.ke

Health insurance premiums differ because people are different.

Different ages.

Different health histories.

Different hospitals.

Different counties.

Different budgets.

Different family sizes.

Different insurance companies.

Different needs.

That is why there is no single medical insurance plan that fits everyone.

Some people need premium hospital access.

Some need family cover.

Some need child-only cover.

Some need senior cover.

Some need group cover.

Some simply need affordable microhealth to protect themselves from sudden hospital bills.

The smartest move is not just buying the cheapest cover.

The smartest move is buying the cover you understand.

For guidance, comparison, and purchase support, talk to Imana Insurance Agency Kenya Ltd or MyKava Online Insurance Consultants.

Call/WhatsApp: +254 113 806 810 | +254 103 806 588

Website: www.imana.co.ke | www.mykava.co.ke

Office: 4th Floor Krishna Centre, Westlands, Nairobi

Compare. Understand. Buy wisely. Protect your health before hospital bills humble your pocket.