Blog Details

Diskava. Beta. Kava

29Nov

Health Insurance in Kenya – Waiting Periods and Other Terms Simplified (2025 Guide)

Confused by "waiting periods" or "co-payments"? We simplify health insurance terms in Kenya to help you find the best medical cover for you and your family.

Let’s be honest—reading an insurance policy document can sometimes feel like trying to decipher a secret code. You see words like "waiting period," "sub-limit," and "co-payment," and your eyes start to glaze over.

But here is the reality: Health insurance in Kenya is one of the most critical investments you will ever make. It is the buffer between your hard-earned savings and a sudden medical emergency.

At Imana Insurance Agency, we believe you shouldn't need a dictionary to understand how your health is protected. Whether you are looking for the best medical cover in Kenya for individuals and families or just trying to understand why you can't use your maternity cover immediately, this guide is for you.

1. The "Waiting Period" Elephant in the Room

This is the number one question we get: "If I buy insurance today, can I go to the hospital tomorrow?"

The answer is yes... and no. This is where the waiting period comes in. Think of a waiting period as a "probation" time. Insurers use it to prevent people from only buying insurance after they get sick (which would make the system collapse for everyone).

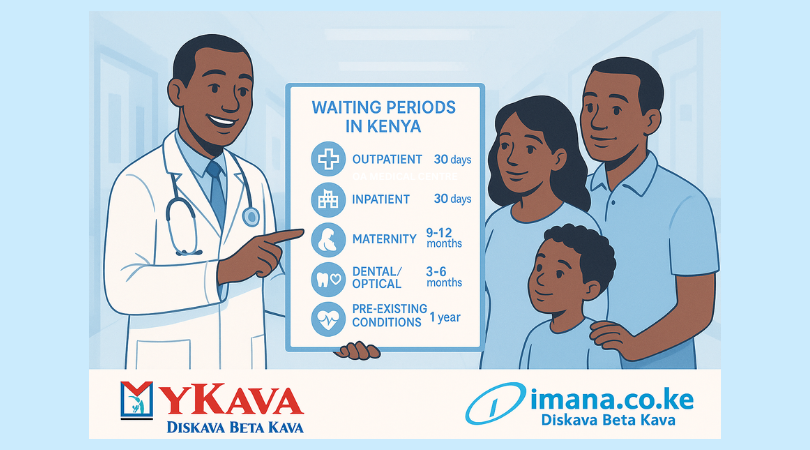

Here is the standard breakdown for most medical insurance companies in Kenya in 2025:

- Accidents (0 Days): Good news! If you are involved in an accident (like a road accident or a fall), you are typically covered immediately from the moment your policy starts. No waiting.

- General Illness (30 Days): For common sicknesses like malaria, flu, or infections, you usually have to wait 30 days after signing up before you can claim. This is always waived if corporate medical scheme.

- Maternity Cover (10–12 Months): This is a big one. Most insurers require you to be on the cover for at least 10 months before you can claim for a delivery. This means you generally need to buy the cover before you conceive.

- Pre-existing & Chronic Conditions (1 Year): If you have a condition like diabetes or hypertension before joining, most insurers will require a 1-year waiting period before they cover expenses related to that specific illness.

2. "Co-Payment": What Does It Mean?

You might see a policy that says "Co-pay: Ksh 500."

This simply means that every time you visit the hospital as an outpatient, you pay a small fixed fee (e.g., Ksh 500) from your pocket, and the insurance pays the rest of the bill.

Why do they do this? It helps keep the cost of your affordable medical insurance in Kenya lower. By sharing a tiny bit of the cost, premiums remain manageable for everyone.

3. Inpatient vs. Outpatient: The Difference

- Inpatient: This is when you are admitted to the hospital and occupy a bed overnight (or for a specific number of hours). It covers the big bills: surgery, accommodation, and doctor’s rounds.

- Outpatient: This covers the "walk-in, walk-out" visits. Consultation, pharmacy drugs, lab tests, and X-rays where you go home the same day.

Pro Tip: When comparing plans on MyKava, you will notice that Inpatient limits are usually much higher (e.g., Ksh 500,000 to Ksh 10 Million) because overnight hospital stays are expensive.

4. "Exclusions": What ISN'T Covered?

No insurance covers everything. "Exclusions" are the specific things your insurer will not pay for. In Kenya, common exclusions often include:

- Cosmetic surgery (unless it's reconstructive after an accident).

- Self-inflicted injuries.

- Experimental treatments.

- Certain supplements or non-medical diet products.

Always check the "exclusions" list before signing. It prevents nasty surprises later!

5. The SHIF vs. Private Insurance Context

With the new changes in government health funding (SHIF/SHA), many Kenyans are asking if they still need private insurance.

The short answer? Yes. While government schemes provide a fantastic base, private health insurance in Kenya offers:

- Access to a wider network of private hospitals.

- Faster service and less congestion.

- Higher limits for specialized care and surgeries.

Think of private insurance as a "top-up" that guarantees you comfort and speed when you are most vulnerable.

6. How to Choose the Right Plan

Don't just look at the price (premium). Look at the value.

- Network: Does the provider cover the hospitals near your home and work?

- Sub-limits: Is there a cap on how much you can spend on things like maternity or dental?

- Reputation: Does the insurer pay claims on time?

Final Thoughts

Insurance doesn't have to be scary or confusing. It is simply a promise that when life happens, you won't have to face the financial burden alone.

Are you ready to look for a cover that suits your budget and needs?

- Compare quotes instantly: Visit MyKava.co.ke to compare the best medical covers in Kenya from top insurers.

- Talk to a human: Need expert advice? Contact Imana Insurance Agency. We are located at 4th Floor, Krishna Centre, Westlands, Nairobi.

Call/WhatsApp us today: +254796209402 | +254745218460. Let’s get you covered!

Disclaimer: Terms and conditions vary between insurers. Always read your policy document carefully.