Blog Details

Diskava. Beta. Kava

11Oct

The Biker's Handbook: Understanding Motorcycle Insurance in Kenya 🇰🇪🏍️

Motorcycles—the swift, efficient backbone of Kenyan transport, from the bustling city commute to the tireless boda boda hustle. While the freedom of two wheels is unmatched, the risks are real. Having the right insurance isn't just a legal requirement; it's the only thing that stands between an accident and financial ruin.

But here’s the critical catch: getting the wrong policy can lead to a rejected claim, leaving you to foot huge bills.

This guide breaks down the common types of motorcycle insurance, highlights crucial policy differences, and addresses a key scenario every rider needs to understand.

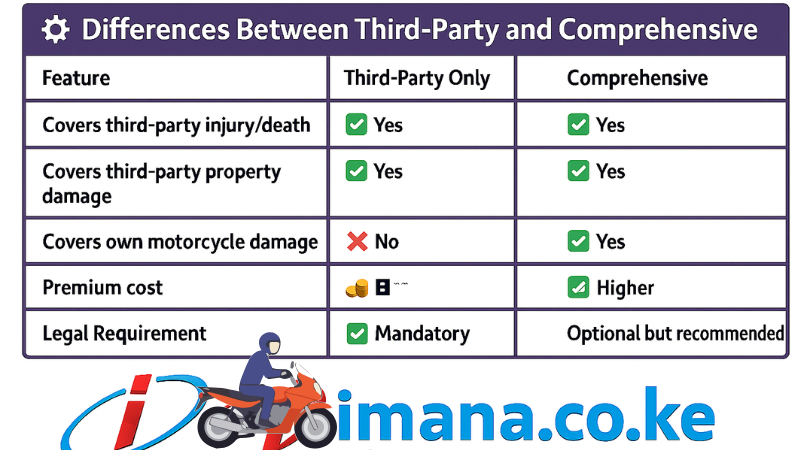

1. The 3 Tiers of Motorcycle Insurance in Kenya

Kenyan insurance companies typically offer three main levels of cover, each providing a different degree of protection:

Policy Type | What It Covers | Who Pays for Your Bike?

1. Third Party Only (TPO) | Covers legal liability for injury, death, or damage to a third party (e.g., the other vehicle, its passengers, or a pedestrian). | You (The policyholder)

2. Third Party, Fire, and Theft (TPF&T) | Covers everything TPO does, PLUS loss or damage to your bike due to fire or theft. | The Insurer (for Fire/Theft only)

3. Comprehensive | The top tier. Covers everything TPO and TPF&T do, PLUS accidental damage to your own motorcycle (e.g., collision, overturning), even if the accident was your fault. | The Insurer (for all covered risks)

💡 Key Difference: TPO vs. Comprehensive

The fundamental difference is straightforward:

Comprehensive protects you, your bike, and the third party, while Third Party Only (TPO) only covers the third party. If you have TPO and crash your bike, the insurer will pay for the damage to the other vehicle, but you will pay for all repairs to your own motorcycle.

2. Usage Classification: The Ultimate Deal Breaker

The most common reason for a rejected claim is a mismatch between the policy's stated "Use" and the actual use during the accident. Insurance is highly sensitive to the risk associated with a bike’s purpose.

Classification | Purpose | Example | Critical Risk Covered

Private | Personal, social, and domestic use only. Not for profit. | Commuting to work, leisure rides. | Low risk (cheaper premium). Excludes PLL.

Commercial | Carrying goods/parcels for business use. No passengers. | Courier services (Uber Eats, Glovo), company deliveries. | Covers third-party risk during deliveries.

Boda Boda (PSV) | Carrying passengers for hire or reward (earning income). | Any typical boda boda service. | Mandatory Passenger Legal Liability (PLL) cover.

3. The Kevin Scenario: A Rejected Claim Waiting to Happen?

Let's look at the scenario: Kevin has a Private Comprehensive Cover, carries a pillion passenger, hits a matatu, and the passenger is injured.

The Claim for the Pillion Passenger's Injury will likely be REJECTED.

Why?

- Wrong Classification: Kevin's policy is for Private Use, meaning the bike is only supposed to carry the rider and is not insured for the liability associated with carrying a passenger, especially if a fee was involved (turning it into a PSV).

- Missing Cover: A standard private policy excludes Passenger Legal Liability (PLL). This is a crucial extension that specifically covers the legal claims and medical expenses of any non-third-party passengers (the pillion). PLL is mandatory for all boda boda (PSV) policies, but it must be added to a private policy if the rider intends to carry any passenger at all.

The Bottom Line: While the Comprehensive part of Kevin's policy would pay to fix his motorcycle and the TPO part would pay for the damages to the matatu, Kevin will be personally responsible for the injured pillion passenger's medical bills and any potential lawsuit, simply because his policy wasn't set up for that risk.

Your Insurance Partner in Kenya

Don't leave your risk to chance. Ensuring you have the correct classification (Private, Commercial, or Boda Boda) and the necessary extensions (like PLL for passengers) is what protects your financial future.

Imana Insurance Agency helps you find the insurance protection that suits your needs and budget, ensuring that it's competitive. We help you get insurance covers from the best insurance companies in Kenya.

Is your car or bike insurance about to expire? We're here to take you through the renewal process and make sure you have the right cover!

Talk to us today!

- Physical Location: 4th Floor, Krishna Centre, Woodvale Grove Westlands - Nairobi Kenya

- Website: www.imana.co.ke or www.mykava.co.ke

- Call/WhatsApp: +254796209402 or +254745218460

Keywords: Motorcycle Insurance Kenya, Boda Boda Insurance, Private Bike Insurance, Comprehensive Motorcycle Cover, Third Party Insurance Kenya, Pillion Passenger Cover Kenya, Insurance Claim Rejected, Insurance Broker Kenya.

#MotorcycleInsuranceKE #BodaBodaCover #ImanaInsurance #RiderSafety #GetInsuredKE #InsuranceAdviceKE #KnowYourPolicy #MyKava #KenyaRiders